Law of “Inocencia Fiscal” – New statute of limitations of 3 years and its application to current tax periods.

On January 2, 2026, Law No. 27,799 (known as the “Tax Innocence Law”) entered into force, which introduces relevant amendments to the Criminal Tax Regime and to the Tax Procedure Law (Law 11,683).

Among the most relevant changes is the reduction of the statute of limitations from 5 to 3 years for certain taxpayers, to determine and demand the payment of taxes, and to apply and enforce fines and closures. The new article 56 of Law 11,683 establishes that:

– The general statute of limitations continues to be 5 years.

– However, it is reduced to 3 years for registered taxpayers who:

1. Have filed the tax return on time;

2. Have paid the resulting balance, if any;

3. Do not register significant discrepancies between the declared amount and the systemic or third party information held by ARCA.

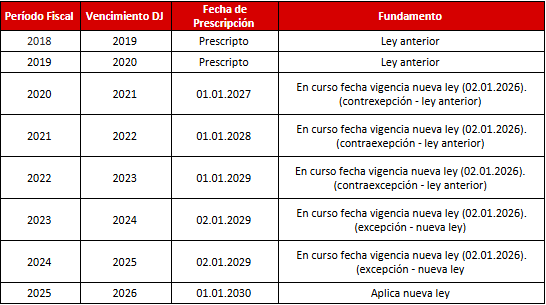

The central issue is to determine whether the new 3-year term applies retroactively to tax periods for which the statute of limitations was already running at the time the law came into effect.

Article 2537 of the Civil and Commercial Code regulates the regulatory transition and states that:

– General rule: current deadlines are governed by the previous law.

– Exception: if the new law sets a shorter deadline, the new deadline counted from its entry into force applies.

– Counter exception: if the deadline set by the previous law expires before the new deadline counted from the entry into force of the new law, the previous one prevails.

General Instruction ARCA No. 3/2026, of internal application for the agency, adopts a criterion in line with the preceding analysis regarding the transitional computation.

Below is a table with the application to each fiscal period.

Law on “Fiscal Innocence” – Guidelines for applying the fines provided for in article 38 of the procedural law

The ARCA, through General Instruction No. 2/2026, establishes the internal procedural guidelines for the application of the fine for taxpayers who fail to file their tax returns (DJ) within the general deadlines set by the Agency under the terms of Article 38 of Law 11,683.

It should be recalled that the so-called Tax Innocence Law updated the amounts of the fine to $ 220,000 for individuals and undivided estates, and to $ 440,000 for companies, associations and other entities incorporated in the country, as well as for establishments organized in the form of stable companies belonging to foreign subjects, as the case may be.

Upon expiration without filing the DJ, a “Reminder for Failure to File” will be automatically generated in the Tax Accounts System (SCT), which will be notified to the Electronic Tax Address (DFE).

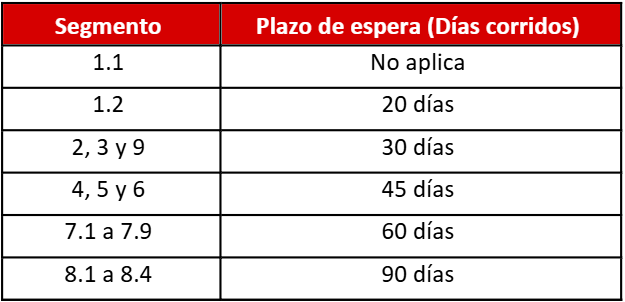

In such reminder, a waiting period will be granted, counted from the due date of the omitted obligation, according to the segment assigned to each taxpayer. This segment may be consulted with the Tax Code through the service “Registration System” → “Registration Data” → “Tax Data” → “Control System”.

Upon expiration of the waiting period, the SCT will register the corresponding fine. In case of persistent non-compliance -i.e., failure to file the DJ and to pay the fine-, the notices provided for both in the SCT and in the Collection Information and Management System (SINGER) will be issued.

Transitional provision In order to allow for the adaptation of the systems, it is foreseen that, for non-compliance between January 2, 2026 and the date of operational implementation, a waiting period of 20 calendar days as from such implementation will be granted, prior to the issuance of the corresponding notices.

If you have any questions or comments, feel free to share them with us:

Cecilia Goldemberg

Managing Partner

cecilia.goldemberg@ar.Andersen.com